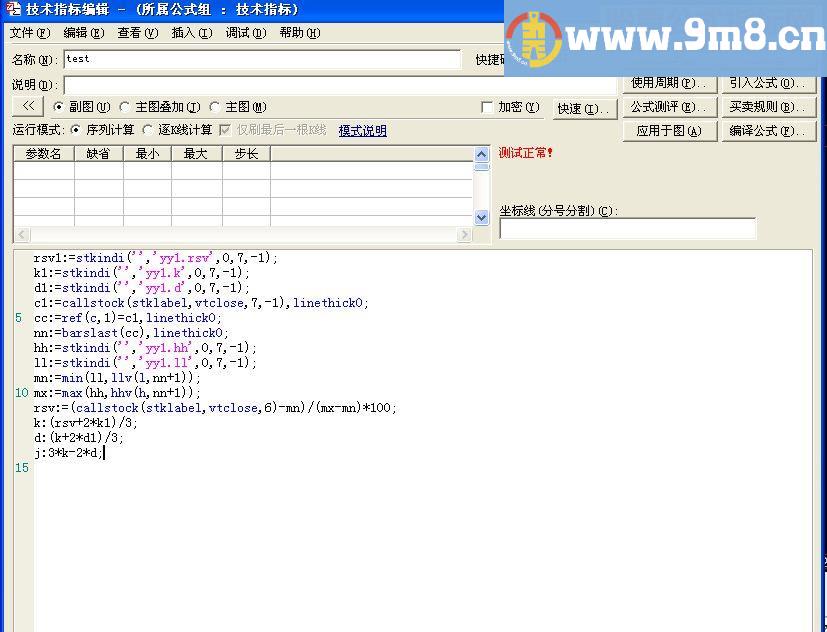

金字塔公式 金字塔模型策略源码:input:period(60,5,120,5);

input:length(20,5,40,5);

input:trailingstop(3,1,6,1);

variable:stopline=0;

topband:=ref(hhv(high,period),1)+mindiff;

botband:=ref(llv(low,20),1)-mindiff;

atr:=ref(ma(tr,length),1);

trailingstopnum:=trimprice(trailingstop*atr);

if holding=0 then begin

if barpos period and high =topband then

buy(1,100%,limitr,close);

end

if holding 0 then begin

if high-trailingstopnum stopline then

stopline:=high-trailingstopnum;

if enterbars =2 and low =stopline then begin

sell(1,holding,limitr,close);

stopline:=0;

end

end

partline(holding 0 and enterbars =2,stopline,coloryellow,1);

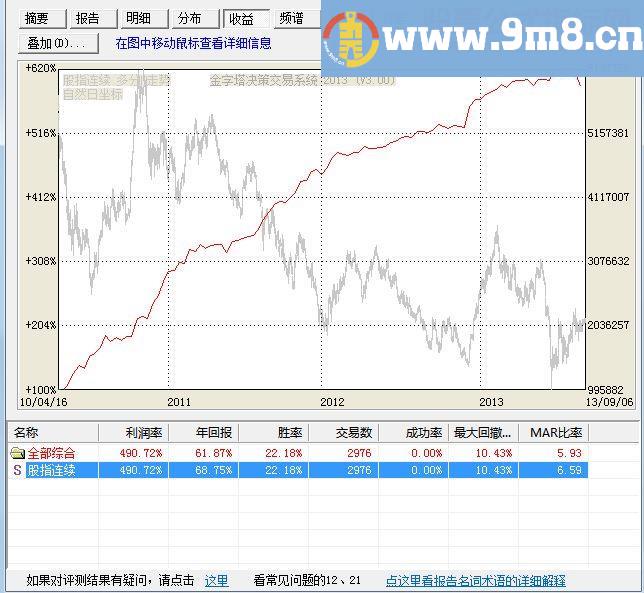

盈亏:asset,noaxis,colormagenta;

收益:(asset-500000)/500000,linethick0;

次数:totaltrade,linethick0;

胜率:percentwin,linethick0;

连亏:maxseqloss,linethick0;

连赢:maxseqwin,linethick0;

复制上述代码粘贴到到公式管理器

源码解析:

输出INPUT:周期

输出INPUT:LENGTH(20,5,40,5)

输出INPUT:TRAILINGSTOP(3,1,6,1)

输出VARIABLE:STOPLINE=0

TOPBAND赋值:昨日周期日内最高价的最高值+MINDIFF

BOTBAND赋值:昨日20日内最低价的最低值-MINDIFF

ATR赋值:昨日真实波幅的LENGTH日简单移动平均

赋值:TRIMPRICE(TRAILINGSTOP*ATR)

逻辑判断 HOLDING=0 THEN BEGIN 逻辑判断 BARPOS 周期 AND 最高价 =TOPBAND THEN BUY(1,100%,LIMITR,收盘价)

STOPLINE赋值:最高价-TRAILINGSTOPNUM

逻辑判断 ENTERBARS =2 AND 最低价 =STOPLINE THEN BEGIN SELL(1,HOLDING,LIMITR,收盘价)

STOPLINE赋值:0

END ENDPARTLINE(HOLDING 0 AND ENTERBARS =2,STOPLINE,画黄色,1)

输出盈亏:ASSET,NOAXIS,画洋红色

输出 收益:(ASSET-500000)/500000,线宽为0

输出次数:TOTALTRADE,线宽为0

输出胜率:PERCENTWIN,线宽为0

输出连亏:MAXSEQLOSS,线宽为0

输出连赢:MAXSEQWIN,线宽为0

![月收益统计功能 和风模板[其他期货软件]](/d/file/p/ad/b1/176867.jpg)